(Tuesday, Sept. 22, 2020; 10:30 PM EST) Covid has suddenly imposed tax and financial obstacles that can make year-end tax planning more challenging in certain situations. Business owners, families with more than $1.1 million in assets in stocks, bonds and real estate, and retirees who take required minimum distributions (RMDs) from an IRA, 401(k), or other qualified retirement account are at risk of missing these major opportunities to reduce their taxes by acting before the end of the year.

Say "No" To RMDs. Individuals who take required distributions from retirement accounts, or who are about to start taking RMDs, may choose to defer their RMD in 2020. With the epidemic keeping you at home, your expenses may be lower in 2020. Deferring all or part of your annual required distribution leaves more invested in a tax advantaged account. This is a strategy for the long term and carries risk but tax-free compounding may make a compelling difference in the terminal value of your account.

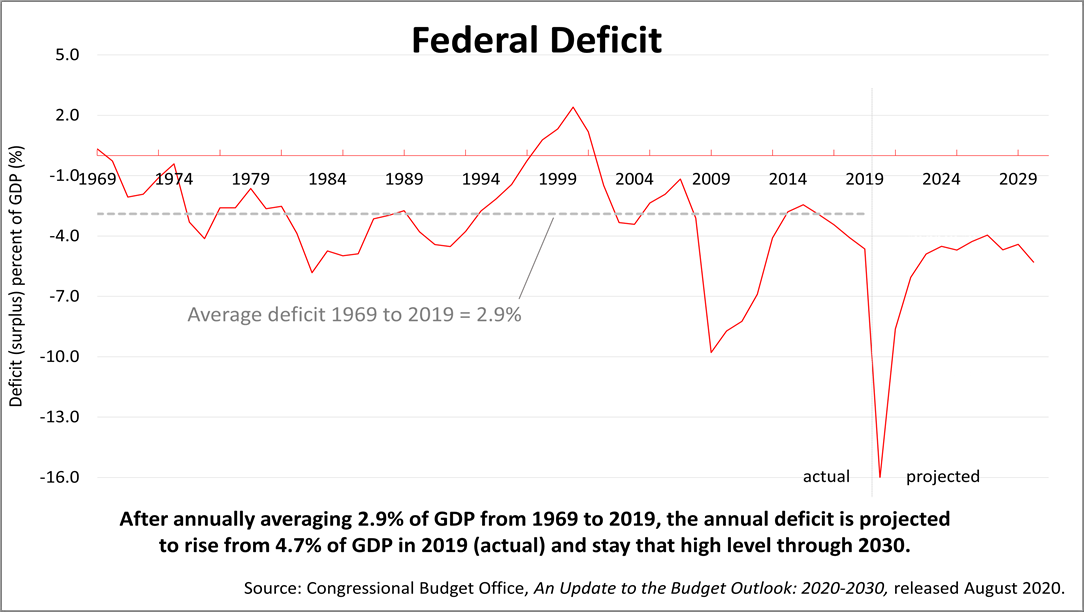

Roth Conversion For 59½-Plus. The federal deficit is soaring this year, due to U.S. government payments of $1200 to qualified individuals, forgivable or subsidized loans to businesses, and $600 monthly additional compensation to the unemployed. This stimulus is widely believed to have saved the economy from a depression but had a cost. To control the rising debt of the U.S., higher taxes should be anticipated. Converting assets in a traditional IRA or qualified retirement account to a Roth IRA makes those assets tax-free for the rest of your life, and benefits your heirs, too. With the stock market falling more than 7% three times in the last six months, now's the time to consider converting assets in traditional IRAs or retirement accounts on the next big stock selloff between now and the end of the year, which acts to reduce the taxes that would be owed on the withdrawal from the traditional IRA later on. The tax- free compounding may make a big difference in your after-tax outcome.

Family Plans. No matter which party wins the election, the estate tax is likely to be increased. Currently, 11.58 million dollars of an individual's estate is not subject to estate tax. While the Trump Administration has not outlined a plan to reduce the spiraling deficit, Joe Biden's plan would cut the estate tax exemption to $1.1 million. Which makes this an opportune moment for families to consider selling property -- like real estate, securities, or interests in private companies -- on an installment-loan basis to children or grandchildren. With interest rates low, the minimum rate on intrafamily loans is low and structuring transactions to give parents (or grandparents) annual income from the sale proceeds for many years can be a smart family plan. Moreover, structuring the sale would maximize lifetime exemption from gift and estate taxes, which can save families from paying estate taxes. You can prepare the documents and you have until October 15, 2021 to decide whether to consummate the transaction , depending on whether the estate tax exemption remains in place after the November 3, 2020 election. |